Los consumidores estadounidenses siguen de pie, pero sienten la tensión

La deuda del consumidor y la dinámica salarial revelan un panorama complejo de resiliencia financiera y vulnerabilidad

Lectura de 6 minutos

PUNTOS CLAVE

- El gasto del consumidor genera casi el 70% del PIB de EE. UU., lo que hace que la salud financiera y la estabilidad laboral sean fundamentales para el crecimiento económico.

- Si bien la deuda total de los consumidores está en niveles récord, los niveles de servicio de la deuda siguen siendo manejables, aunque la tensión se distribuye de manera desigual entre los grupos de ingresos.

- El crecimiento de los salarios se ha desacelerado para las personas de bajos ingresos, lo que contribuye al aumento de la morosidad.

La salud del consumidor estadounidense es de suma importancia cuando pensamos en el crecimiento económico futuro, ya que aproximadamente el 70% del producto interno bruto (PIB) de los Estados Unidos se basa en el gasto del consumidor. Recientemente, la Reserva Federal pasó de centrarse en la inflación a centrarse en las señales de debilidad en el mercado laboral, lo que resalta la importancia de la salud financiera de los consumidores. Cualquiera que sea el entorno, un consumidor con un trabajo y confianza en su situación laboral es mucho más probable que gaste que un consumidor con poca confianza o sin trabajo.

Sin embargo, incluso tener un trabajo no significa que todo sea color de rosa. Los gráficos y comentarios anteriores han señalado la bifurcación de los consumidores en función de los cuartiles de ingresos, así como el hecho de que la inflación afecta más a las personas que no poseen activos financieros, como una casa y acciones. Con esto en mente, nuestros gráficos de esta semana analizan a los consumidores desde un par de perspectivas diferentes, incluidas sus deudas y ganancias.

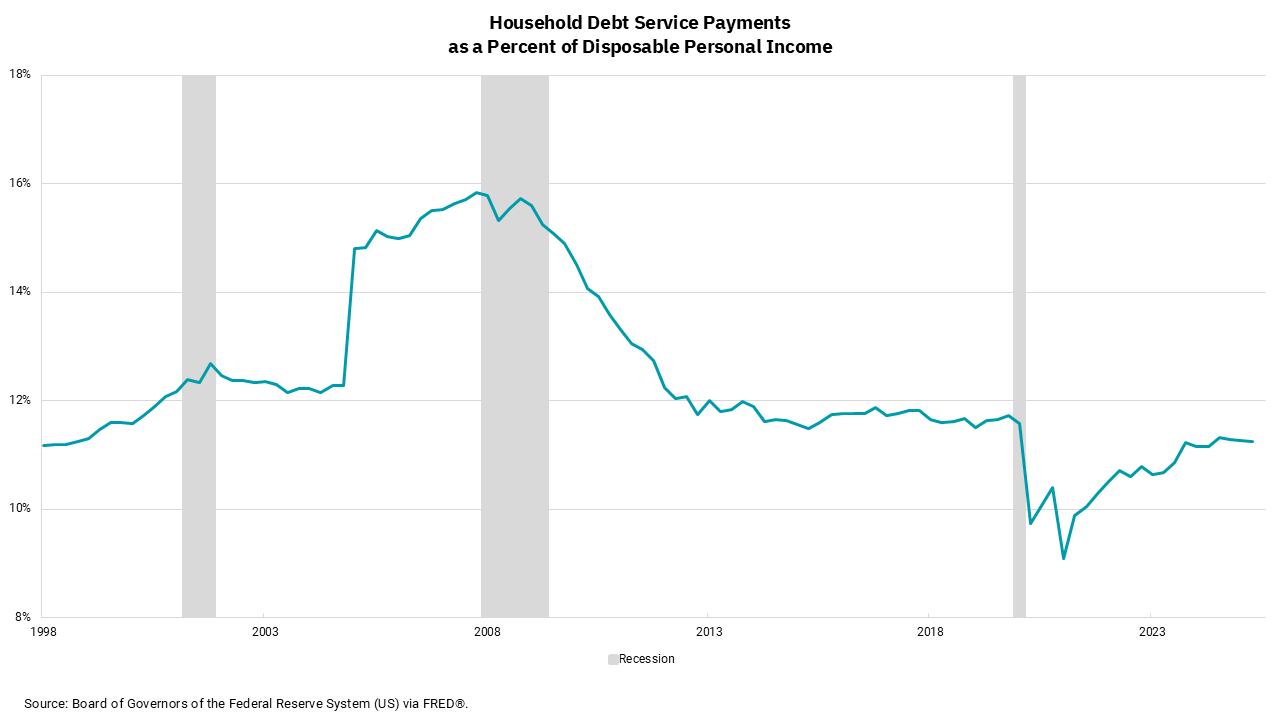

Los niveles totales de deuda del consumidor, que abarcan hipotecas, préstamos estudiantiles, préstamos para automóviles y tarjetas de crédito, están en niveles récord. Eso, en sí mismo, no es malo, ya que esperaríamos que fuera cierto dentro de una economía en crecimiento. Y está creciendo: la producción bruta de la economía estadounidense está en niveles récord. También sabemos que no es solo el nivel de deuda, sino el costo de esa deuda lo que importa. Nuestro gráfico superior trata de ver cómo el nivel y el costo de la deuda general del consumidor se compara con períodos anteriores. Lo que vemos es un consumidor estadounidense que está en peor estado de lo que estaba después de billones de estímulos mientras superábamos la pandemia, pero que todavía está en mejor forma que cuando entramos en la pandemia y materialmente mejor que el período previo y durante la crisis financiera. Esta es una imagen general, por lo que sabemos que dentro de estos datos hay consumidores que están mejor y peor, pero en conjunto, el consumidor estadounidense está bien desde el punto de vista del servicio de la deuda.

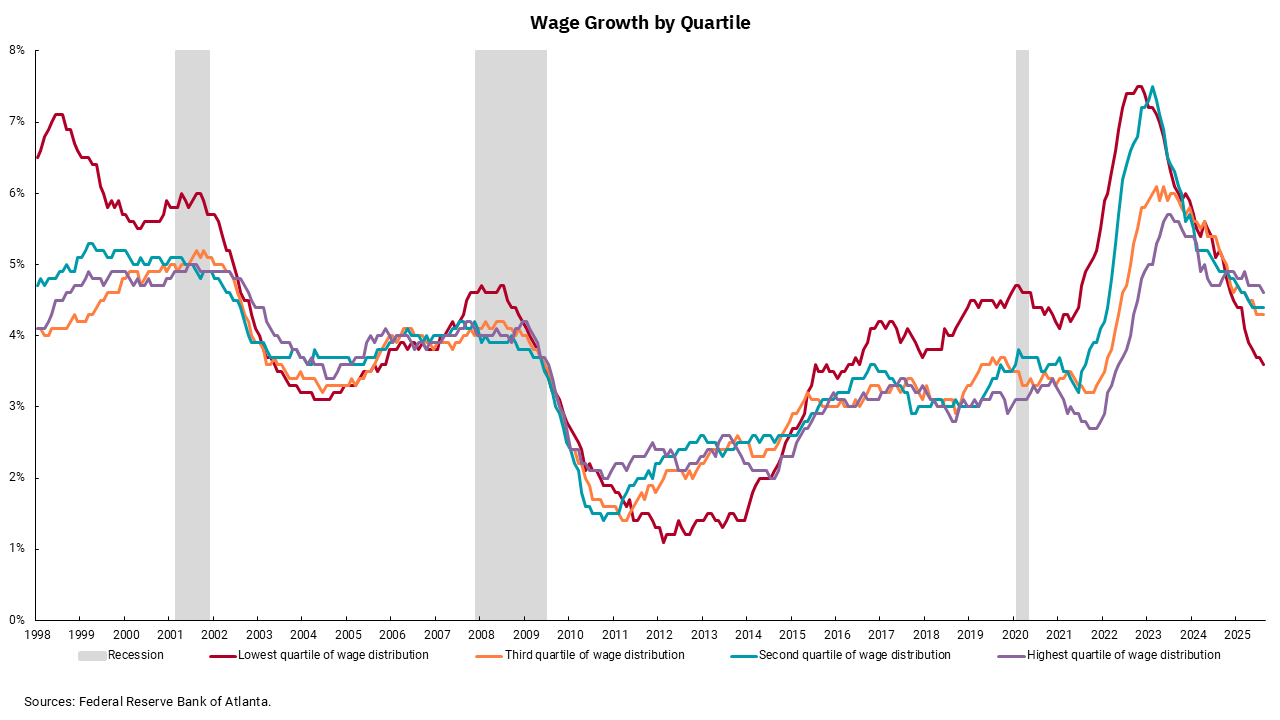

El gráfico inferior ayuda a proporcionar cierta claridad sobre las diferentes posiciones del consumidor estadounidense. En este gráfico, observamos el crecimiento salarial por cuartil de ingresos. Al salir de la crisis financiera y luego a través y fuera de la pandemia, vemos un período en el que el quintil salarial más bajo estaba obteniendo ganancias salariales desmesuradas en comparación con otros quintiles de ingresos. Eso fue particularmente cierto ya que los planes de estímulo del gobierno estaban en vigor, y vimos dos puestos de trabajo abiertos por cada persona desempleada. Puede que no sepa esto, pero la tasa de salario mínimo federal sigue siendo de $ 7.25 / hora. La tasa de salario mínimo "efectiva", sin embargo, es significativamente más alta que eso.

En los últimos años, hemos visto que las ganancias salariales convergen en los quintiles de ingresos, y recientemente, las ganancias salariales del quintil de ingresos más bajos han comenzado a retrasarse. Esto ayuda a explicar por qué la morosidad por ingresos y puntaje FICO está aumentando más rápido para puntajes y niveles de ingresos más bajos. De estos datos deduzco dos cosas: primero, sigue siendo importante que la Fed trabaje para que la inflación vuelva a su objetivo del 2%. En segundo lugar, también es importante tomar medidas para proteger el mercado laboral. Desafortunadamente, hacer ambas cosas al mismo tiempo es difícil. Por ahora, el enfoque de la Fed es el mercado laboral.

Obtenga By the Numbers en su bandeja de entrada.

Suscríbase (Se abre en una pestaña nueva)