Los consumidores "definitivamente" van a experimentar precios más altos

La brecha entre las ganancias salariales agregadas y la inflación puede ampliarse nuevamente

Lectura de 5 minutos

PUNTOS CLAVE

- Las lecturas recientes del IPC y el PCE cumplieron con las expectativas, pero los mayores costos de la energía y los alimentos están impulsando la inflación general.

- Si bien la moderación de los costos de la vivienda mantiene bajo control la inflación subyacente, es poco probable que los consumidores sientan mucho alivio.

- El aumento de los precios amenaza con reabrir la brecha entre la inflación y los salarios, con el mayor impacto en los hogares de bajos ingresos.

Lecturas recientes de inflación de la Índice de Precios de Gastos de Consumo Personal (PCE) y el Consumer Price Index (CPI - Índice de Precios al Consumidor) entró como se esperaba. Esa es una buena noticia. La mala noticia, sin embargo, es que las expectativas ya reflejan el comienzo de un aumento de la inflación basado en los mayores costos de energía del conflicto en Irán. La inflación general está siendo liderada por un aumento masivo en los precios de la gasolina y el aumento del costo de producir y distribuir alimentos. Dado que los mayores costos de los fertilizantes afectan los costos de producción, esperamos que los precios de los alimentos muestren una mayor presión al alza en los próximos meses.

Es importante destacar que sabemos que la Reserva Federal elimina los alimentos y la energía de la ecuación y observa más de cerca la tasa "básica" de inflación. En ese frente, el principal impulsor de la inflación son los costos de la vivienda, y aquí vemos una moderación continua en los alquileres que está permitiendo que la tasa de inflación subyacente muestre aumentos más moderados. Según el informe del IPC del viernes, la inflación general ha subido un 3,3% interanual, mientras que la inflación subyacente ha subido "solo" un 2,6%. Esto puede ser un presagio de lo que vendrá, ya que la inflación general muestra una mayor presión al alza durante algún período de tiempo.

Desde la perspectiva de la Fed, las lecturas moderadas de inflación subyacente y las expectativas de inflación a largo plazo estables y continuas pueden proporcionarles la cobertura para no aumentar las tasas. Aún así, los consumidores definitivamente sentirán el pellizco de los precios más altos.

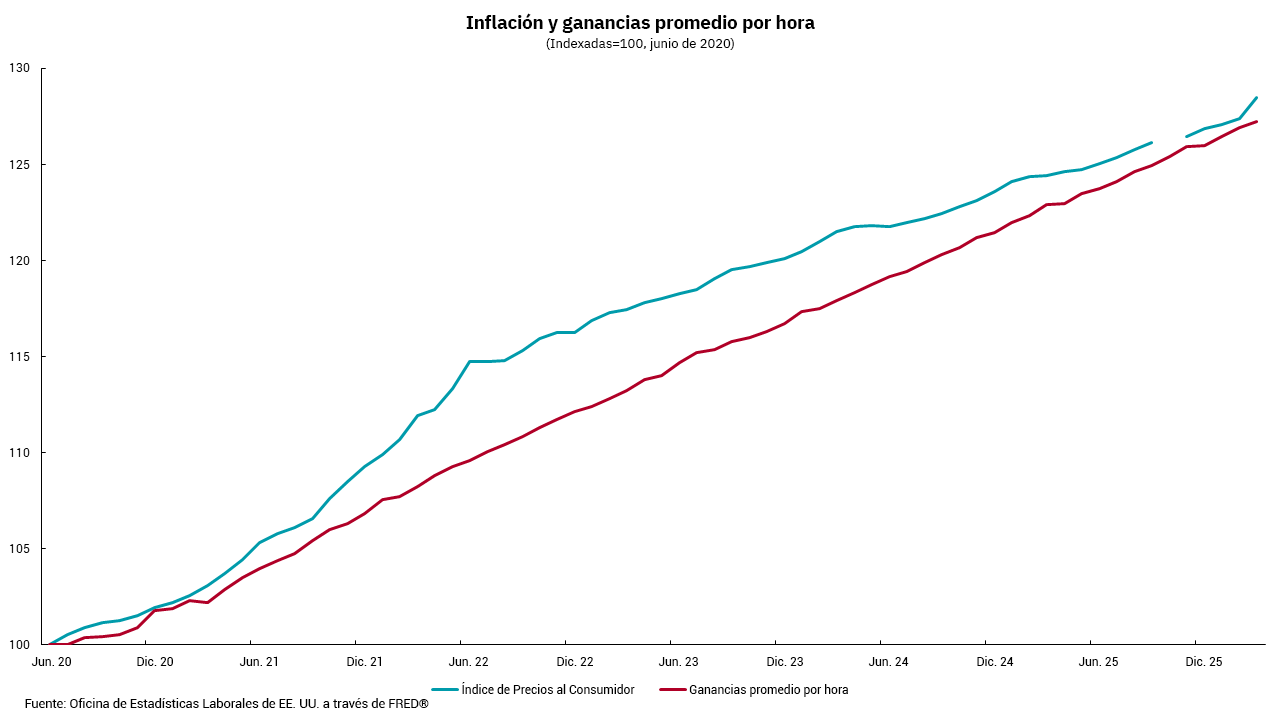

Con eso en mente, nuestro gráfico de esta semana es uno que hemos usado a menudo. Muestra las ganancias de la inflación agregada en el IPC en comparación con las ganancias salariales agregadas que se remontan al inicio de la pandemia. Estados Unidos acababa de comenzar a hacer algunos progresos en el cierre de esta brecha, ya que la inflación se desaceleró y las ganancias salariales fueron más altas que los aumentos de precios.

Sin embargo, ahora parece que el conflicto en Irán va a ampliar esta brecha en el futuro. Todos sentimos el impacto de los precios más altos, pero los grupos de ingresos más bajos lo sienten más agudamente. Esto se debe principalmente a que los grupos de ingresos más bajos gastan una mayor proporción de sus ingresos en artículos como alimentos y gasolina. Las implicaciones de esta nueva ampliación son tanto económicas como políticas. No hay un solo punto de datos económicos con una correlación más alta con el índice de aprobación de un presidente que los precios de la gasolina. Y aunque la brecha entre la inflación y los salarios se había ido reduciendo, todos sentimos el impacto en áreas como las facturas de calefacción del hogar y los seguros, donde los costos han aumentado significativamente más rápido que las tasas de inflación general.

En resumen, si bien la Fed podría evitar aumentos de tasas a medida que miran hacia el próximo período de precios más altos, los consumidores van a sentir el pellizco. Todo esto se prepara para lo que podría ser un electorado gruñón en las elecciones de mitad de período. Y siempre es así, si los votantes no están contentos, el partido en el poder, que actualmente es el Partido Republicano, va a pagar un precio en las urnas.

Obtenga By the Numbers en su bandeja de entrada.

Suscríbase (Se abre en una pestaña nueva)