How ultra-low-rate mortgages reshaped the housing market

Previous Fed policies had good intentions, but left today’s market divided between current owners and new buyers

Lectura de 5 minutos

PUNTOS CLAVE

- Years of ultra low rates and pandemic era Fed support have locked millions of homeowners into mortgages they can’t afford to give up.

- Existing home sales, not new construction, remain the biggest drag on housing affordability and supply.

- First time buyers increasingly must rely on family help to enter an uneven market.

The housing market can't seem to catch a break. Just as 30-year mortgage rates broke below 6% for the first time since 2022, the conflict in Iran led to surging oil prices, higher rates and removed any chance of lower rates from the Federal Reserve in the short- to intermediate-term. The timing of something like this can never be good, but happening just as the important spring homebuying season was getting started would seem to be especially cruel.

The reasons for the dysfunctional market are varied but both have to do with the Fed’s rate setting policies—namely, the extended period of ultra-low rates, followed by the Fed’s extraordinary support during the pandemic.

Taking a closer look at the second factor: During the fourth round of quantitative easing (QE4), which began in 2020, the Fed bought billions in mortgage-backed securities to stabilize markets, which sent mortgage rates to record lows. While the intent was good, it introduced a level of distortion within the market to which we are still paying a price.

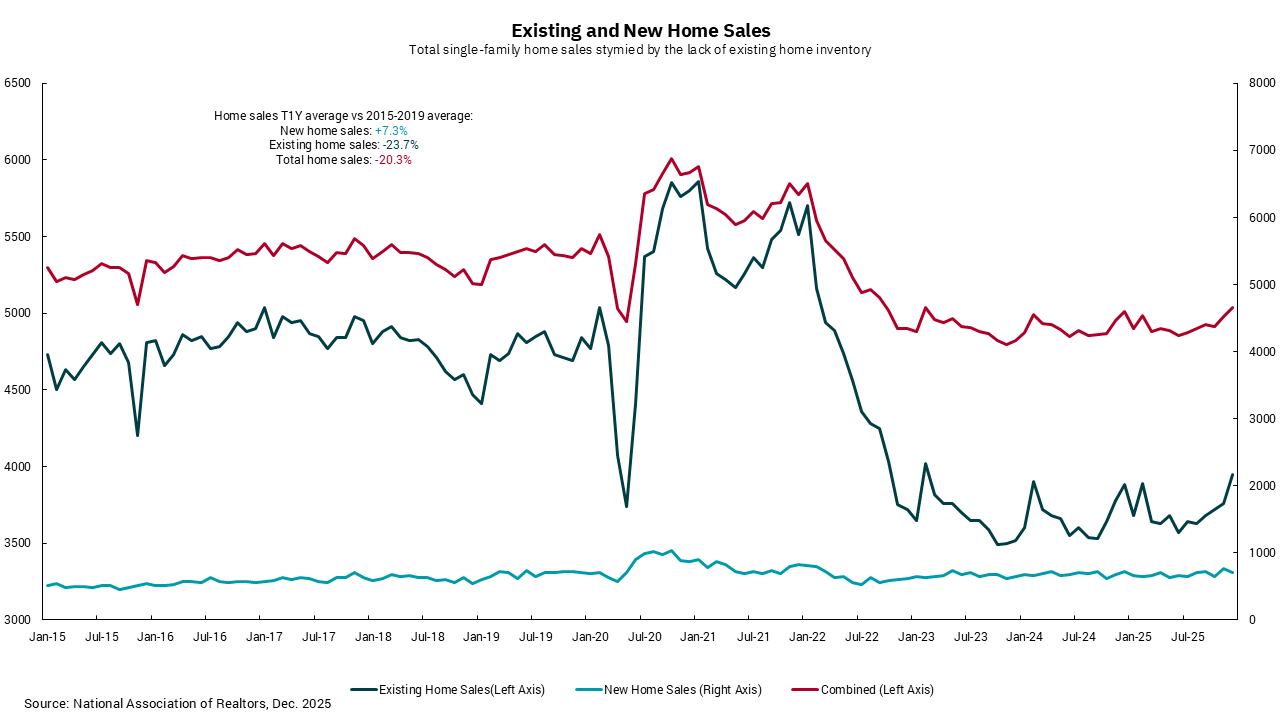

Our chart this week shows new home sales, existing home sales and total home sales. As the chart shows, the biggest change in the housing market has been the downshift in existing homes sales. New home sales have been relatively stable with a measurable increase based upon the aforementioned rate and QE policies, but the real volatility has been in existing home sales. Importantly, the existing home sales market has always been the biggest part of the equation. A longer-term chart would show a downshift in new homes as the economy recovered from the Great Financial Crisis, but existing homes are the crux of the issue.

As Christopher Maloney, a mortgage strategist with BOK Financial Capital Markets put it- "Another contributing factor to the paucity of existing home sales comes from the Fed's ultra-aggressive monetary policy during QE4, which sent mortgage rates to record lows. So, as of this time, 53% of the unpaid balance on all 30-year conventional and Ginnie Mae mortgages sport rates of 4% or less. That's a total of 17.7 million homeowners who are not about to move (or refinance) anytime soon."

In many ways the housing market is bifurcated. For those already in the housing market, it is hard to see what the problem is. Many have fixed-rate mortgages with low rates and materially higher home values. However, for anyone trying to get into the housing market, it is a mess.

This mess isn't because there has been a lack of ideas on what might be done from a federal government standpoint. These ideas have included: restricting single family home purchases by private equity firms, 50-year mortgages, mortgage portability, opening federal lands for construction, rent controls, additional tax incentives, increased domestic timber production, additional purchases by Ginnie Mae (GNMA) and Fannie Mae (FNMA) and a new tax credit for home ownership.

However, real solutions must address both supply and demand. In the meantime, many first-time homebuyers, who now average 40 years of age, will be getting help from their parents or grandparents to buy a home.

Obtenga By the Numbers en su bandeja de entrada.

Suscríbase (Se abre en una pestaña nueva)